Salesforce (CRM) Stock Analysis 2026: Earnings Beat, AI Growth & Is This a Buying Opportunity?

CRM stock surged after earnings — but volatility continues.

Agentforce AI revenue is accelerating at triple-digit growth.

Is the software sector bottoming — or is uncertainty still ahead?

advertisement

Salesforce (NYSE: CRM) stock is back in the spotlight after delivering a strong earnings report that beat Wall Street expectations, reigniting debate over whether enterprise software stocks have finally reached a bottom in 2026.

Despite posting impressive growth numbers, announcing a massive $50 billion buyback, and showcasing explosive AI momentum, the market’s reaction has been mixed — highlighting both opportunity and lingering fear in the sector.

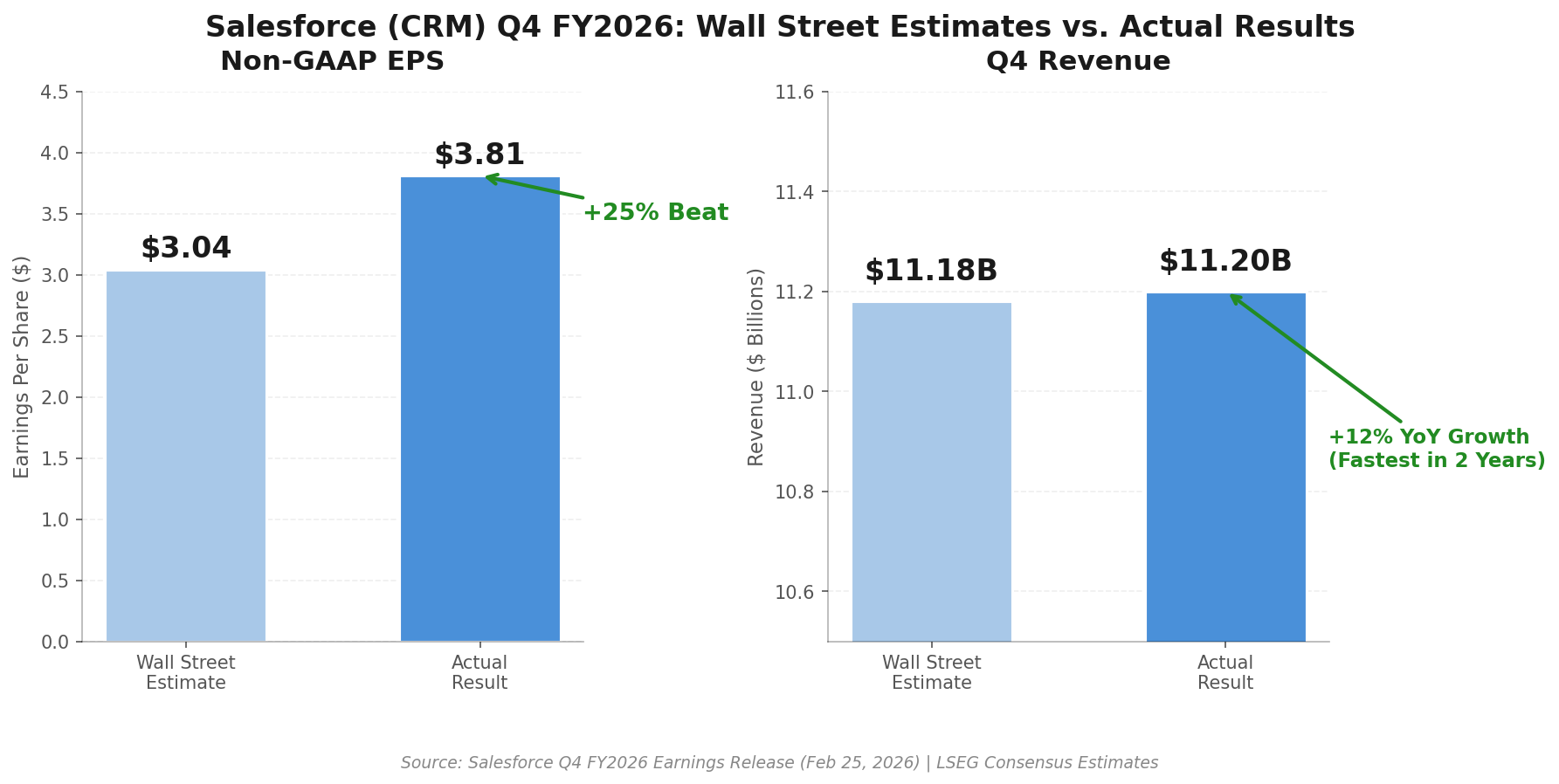

Salesforce reported fourth-quarter revenue of $11.2 billion, up 12% year-over-year — its fastest growth rate in two years, according to Investing.com.

Non-GAAP EPS came in at $3.81 versus the $3.04 analysts expected — a 25% earnings beat.

Full-year revenue reached $41.5 billion, surpassing the $40 billion milestone for the first time, while operating cash flow climbed 15% year-over-year to $15 billion.

The company also reported $72 billion in total remaining performance obligations, up 14% year-over-year, reflecting strong long-term demand visibility.

Yet, despite these results, CRM shares initially dropped about 4% premarket, as noted by Investing.com.

The reason? Fiscal 2027 revenue guidance of $45.8–$46.2 billion came in roughly in line with analyst expectations — strong, but not the upside surprise investors were hoping for in a risk-sensitive environment.

advertisement

Meanwhile, Barron’s reported that Salesforce stock rebounded 3.5% to $198.39 during regular trading, helping lift the broader software sector.

The iShares Expanded Tech-Software Sector ETF rose 2.2% that day and has gained 7.4% over three sessions — its best three-day stretch since April 2025.

However, the ETF remains down 30% from its September 2025 high, underscoring how deeply the sector has been sold off amid fears that artificial intelligence could replace traditional software tools.

At the center of Salesforce’s strategy is Agentforce — its enterprise AI platform.

According to the company, Agentforce’s annual recurring revenue reached $800 million in the fourth quarter, up 169% year-over-year.

Combined Agentforce and Data 360 ARR totaled $2.9 billion, rising more than 200% year-over-year.

Salesforce closed 29,000 Agentforce deals in just 15 months, up 50% quarter-over-quarter.

CEO Marc Benioff emphasized strong demand, describing Agentforce as an "$800 million business" and dismissing the so-called "SaaSpocalypse" fears during the earnings call.

These numbers suggest Salesforce isn’t being disrupted by AI — it’s monetizing it.

Still, uncertainty remains.

Morgan Stanley analyst Keith Weiss described certain forward-looking metrics as “disappointing” relative to expectations for a beat, particularly current remaining performance obligations growth.

Barron’s quoted Ameriprise strategist Anthony Saglimbene as saying it’s “too soon to tell” whether the SaaS downturn is over, though opportunities may be emerging for investors willing to tolerate volatility.

James Demmert of Main Street Research told Barron’s that best-of-breed software stocks such as Palantir Technologies, Microsoft, and Salesforce appear “very oversold and have likely bottomed.”

Nancy Tengler of Laffer Tengler Investments took a more cautious stance, noting that while Salesforce will remain a major player, its future growth rates may not match its historical trajectory.

advertisement

Adding another layer to the debate, Jensen Huang of Nvidia publicly pushed back against fears that AI agents will replace enterprise software.

He argued that AI agents will actually become heavy users of software tools, calling the current market narrative a “deep misunderstanding.”

If Huang is right — and if HSBC analysts are correct in predicting that 2026 could mark the beginning of large-scale enterprise AI monetization — software companies like Salesforce may capture significant value in the next AI wave.

So, is CRM stock a hidden buy signal?

The company delivered a 25% earnings beat, accelerated AI-driven revenue growth, crossed $40 billion in annual sales, generated $15 billion in cash flow, and announced a $50 billion buyback.

Yet shares remain pressured by macro uncertainty and skepticism around future growth.

The disconnect between fundamentals and price action is precisely what long-term investors look for — but only if they believe the AI transformation will enhance, not erode, software demand.

Conclusion: A Sector at an Inflection Point

Salesforce’s latest earnings suggest something important: enterprise software may not be collapsing under AI disruption — it may be evolving through it.

The panic-driven selloff across software stocks reflects uncertainty, not necessarily deterioration.

If AI agents truly rely on — and amplify — enterprise software platforms, companies with scale, recurring revenue, and proven monetization models could emerge stronger than before.

Whether 2026 marks the definitive bottom for CRM stock and the broader software sector remains uncertain.

But history shows that transformative technology cycles reward companies that adapt early and execute well.

Salesforce has made its bet on AI.

The market now must decide whether it believes the strategy will pay off.

Key Points

Salesforce delivered a 25% EPS beat and crossed $40B in annual revenue.

Agentforce AI revenue is growing at triple-digit rates.

Software stocks may be stabilizing, but volatility remains high.

advertisement

Frequently Asked Questions (FAQ)

1. Why did Salesforce stock drop despite strong earnings?

Although Salesforce beat earnings estimates, its fiscal 2027 revenue guidance was only in line with expectations, which disappointed investors seeking stronger forward momentum.

2. What is Agentforce and why does it matter?

Agentforce is Salesforce’s AI platform designed to enhance enterprise productivity. Its rapid ARR growth suggests strong adoption and positions Salesforce to monetize AI demand.

3. Has the software sector hit bottom?

Some strategists believe leading software companies are oversold and may have bottomed, while others caution that volatility and AI competition remain risks.

4. Is CRM stock a buy in 2026?

Analysts are divided. Bulls see strong fundamentals and AI monetization. Cautious investors want clearer signs of sustained growth acceleration.

Sources

- Barron’s – Analysis of Salesforce earnings and software sector rebound

https://www.barrons.com/articles/salesforce-stock-earnings-software-bottom-4e96595d - Investing.com – Earnings beat analysis and AI-driven buy signal discussion

https://www.investing.com/analysis/salesforce-delivered-a-25-earnings-beat-and-still-slid--a-hidden-buy-signal-200675736

Thank you !